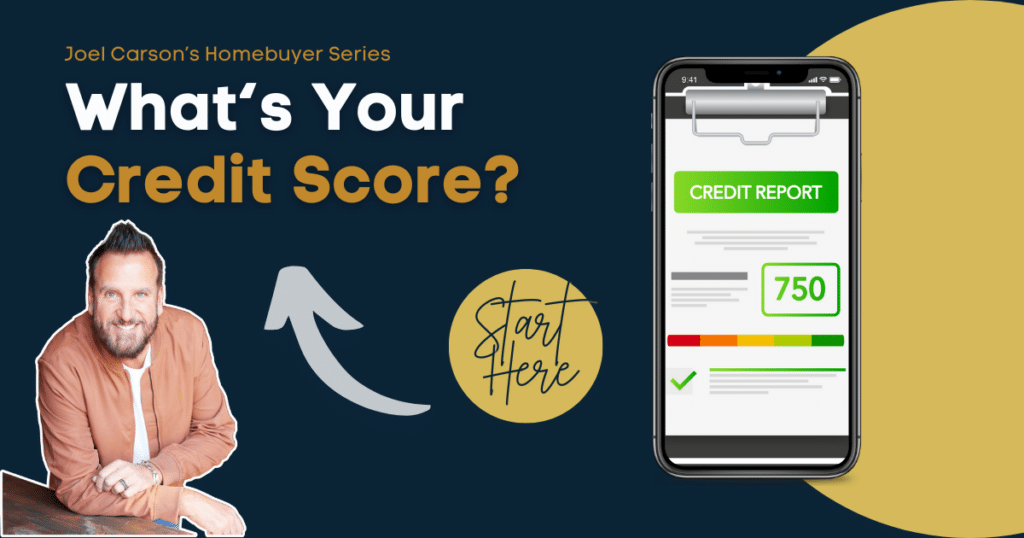

Know how your credit score impacts purchasing power

Your credit score is taking shape today even if you are years from buying a home. Don’t panic but yes, there will be a test after this. Your score will become your “credit score,” and it will follow you for the rest of your life.

A credit score is a number many lenders use to determine the likelihood that you will pay back the money you borrow. It’s part of a multi-part risk assessment. That might be an oversimplification but it boils down to how much you can afford to borrow and how likely you are to pay it back.

Credit scores range from 300 to 850. Conventional home loans require a credit score of 620 or higher. Many loan programs can work with lower scores, but there are added expenses and restrictions for high-risk buyers.

Do you know where you are on the scale?

- 800 to 850: Excellent. Individuals in this range are considered to be low-risk borrowers.

- 740 to 799: Very good

- 670 to 739: Good

- 580 to 669: Fair

- 300 to 579: Poor

The score is a mathematical sequence made up of multiple factors. These credit scoring models include:

- your payment history

- your current unpaid debt

- the number and type of loans you have

- the ages of your accounts

- the amount of credit you are using compared to the amount of credit you have

- how many times you apply for credit

- public records that indicate

- collections

- foreclosures

- bankruptcies

- judgments

- liens

You can directly impact your credit score

A good credit score is a valuable asset. Tend it like you watch your bank account numbers change. People with high credit scores are low-risk borrowers, so they pay lower interest rates than high-risk lenders. Lenders are most commonly associated with credit scores but employers and others use them too as a measure of character.

First: You need credit to have a credit score

Some people prefer cash-only living. That is one sure way to avoid debt if your cash flow is steady and strong (and you live within your means). Unfortunately, if a situation does require you to borrow money, you might not be able to get it. Lenders want to know you are capable of using credit responsibly and consistently.

Apply for a credit card, and find a landlord who reports to a credit bureau. Buy a car on credit, and ask if your utility companies report to credit bureaus. It is important to establish a solid credit history.

Second: Understand lender agreements and honor them

If you have a credit card, use it regularly. Make payments on time. It’s best to carry a balance of around 30%.

Third: Don’t close revolving credit accounts when they are paid

The age of your credit history is a factor in your credit score. So is available credit. Leave those accounts open, use them from time to time, and it will bolster your credit. These are just a few of the ways you can improve and maintain your credit score. Some businesses specialize in credit repair. Check reviews and research a company’s reputation before hiring one.

Get a free copy of your credit report

FICO is one of the most popular scoring systems used by mortgage lenders today. You are entitled to a free copy of your credit report annually. Following are links to the top three reporting agencies in the United States. Borrowing money to buy a home is one of the most important financial decisions you will make. Start building or restoring your credit profile now.

Pre-mortgage planning paves the way

The yellow brick road to owning a home is paved with preparation. You might not be ready to jump into home ownership today. That’s okay. It’s never too early to plan your strategy. Most first-time buyers need to secure financing from a mortgage lender. Having your important documents in order will save you, the buyer, undue stress, time, and frustration when you do finally leap.

Building an “Important Documents” file will make your life easier on so many levels. Have you ever scrambled through your house looking for a lost birth certificate, an official marriage license, immunization records, or a canceled check? It’s mind-numbing to frantically search for a passport, vital records, annual taxes, college transcripts, your degree, etc. Spare yourself those few minutes (or many hours) of panic. Start gathering these things today.

Your “I know where everything is, just don’t touch my desk,” method might work perfectly for you, but in the unlikely event you become incapacitated, would it make sense to someone else? Maybe that green garbage bag has been the only filing system you’ve needed for years. Or maybe you’re one of those, “It’s somewhere in my mom’s attic,” record keepers. Before you embark on the mortgage application process, it’s time to find a better way. There is no time like the present.

Build a living mortgage file

Keep a secure electronic copy of your important documents. Following are some pros of digital records:

- They take up less room than hard copies.

- They’re easy to search.

- They are environmentally friendly.

- Back-up files are easy to make, store, and share.

There are some real cons to using only digital storage too:

- Security is critical and constantly changing.

- Some institutions require original hard copies.

- Piling up paper in an “I’ll Scan this Some Day” file does not constitute a system.

- Technology changes. Your thumb drive files might not be accessible in 10 years.

Create a digital and a hard copy filing system and protect both with security that makes sense. Document safes are available online starting at just more than $50. These make great storage for vital records and protect them from fire, water, wind, and prying eyes. They are not fail-proof.

The format in which you save digital files matters. If you put them on a thumb drive or CD, they will still be vulnerable and likely in the same building where you store hard copies. If you do store files on external drives, keep them in a different location (like, miles away) from your hardcopies. Disasters strike. If one set of documents is destroyed, the other is likely to survive.

Review technology annually and determine if your file formats and storage methods are in keeping with modern standards. Upgrade when necessary.

There are many cloud-based programs available for storage. Research multiple options. Read reviews, understand security measures, and check the health of the company you choose to be the keeper of your life library.

When you organize your critical documents, organize them in a standard format that almost anyone can understand. Remember:

- Use separate file folders for each set of documents. Organize them by individuals, contents, or by subject.

- Label file folders with a bold marker or bold-face type.

- Alphabetize folders.

- Store hardcopy documents in a clean, dry, place with moderate temperatures.

- Protect documents in acid-free storage sleeves.

- Shred and discard outdated records.

Your hardcopy files will include:

- passports

- Social Security Cards

- insurance Policies

- life

- auto

- health

- property

- birth certificates

- death certificates

- marriage/divorce records

- stocks and bonds

- immunization records

- emergency contacts and complete contact information

- court orders

- tax records

- some bank records

- titles

- deeds

What do immunization records have to do with a mortgage application? Well, nothing. As long as you are starting a file, let’s get these ducks in a row so you don’t have to waste your time herding them around (when you could be focusing on your dream of owning a home).

This file should remain fairly small, simple, and clear. Find one trustworthy person who does not live with you. Share the code/key/combo with a trusted confidant.

What kind of documents will your lender require?

Following is a list of documents your lender might require when you apply for a mortgage:

- state-issued identification, a passport, or a U.S. alien registration card

- income information and supporting documentation

- bank statements

- investment account statements

- rental information & documentation

- a list of your debts and the most recent statements for example:

- tax documents

- car loans

- student loans

- credit cards

- personal loans

- home insurance policies

- Homeowners Association (HOA) information

- medical bills

Many of these documents must be current (the most recent). If you electronically file statements they should be readily available. Most are easy to get from the service provider, agency, lender, etc. within 24 months (check with your institution). Make a list of current/past accounts. Include Names, account numbers, websites, email addresses, and passwords. This will help you gather these items quickly when you need them. Keep a copy of your hardcopy documents.

You pay your bills on time. You exercise your credit (but not too much). You monitor your credit score and it’s looking good. You have a stellar “Important Papers” filing system. Now, you’re ready to begin the home-buying process!

You’ve already done the hard part. It’s time to apply for mortgage preapproval. In a competitive market, this is especially important. Homeowners get multiple offers on one property. They will consider those buyers with cash or a loan preapproval more favorably than a potential buyer without one.

Get a ‘Letter of Preapproval’

Your mortgage lender will generate a Letter of Preapproval when the lender determines you are creditworthy. The lender you choose will evaluate your application, check your credit report, and review your debt-to-income ratio. The lender might ask for some verification too. If your financial life appears to be in order, the lender will give you a Letter of Preapproval. The letter should also state the type(s) of loan(s) for which you qualify and the amount you can borrow for a home.

A Letter of Preapproval does not guarantee your loan. Circumstances change, and sometimes information is unverifiable. Failure to prove you have the funds to make a down payment and closing costs can be a deal-breaker (and a heart-breaker). Always tell the truth when filling out an application. Never overstate income or understate debt.

It can take an hour to months to get pre-approval. Yours will move fast because you’ve got all your ducks lined up, and you have dealt with the Ghost of Credit Past.

Find a Realtor

With your letter of pre-approval in hand, interview three Realtors. Ask about their experience in your market. Compare their gross sales in the last year. Compare the number of transactions they closed during that time. Also, check reviews online. With 269 reviews on Zillow, I maintain a 5-star rating in local knowledge, process expertise, responsiveness, and negotiation skills (a 5-star rating overall). The pressure is on agents today more than ever. Their commitment to serving buyers and sellers is frequently reflected in their reviews. Choose wisely.

Shop until you drop

By now you have a Letter of Preapproval and a great Realtor. It’s time to look at homes! Shop for homes in your price range and chosen location. Not all homes qualify for all loans, so clarify whether yours will be a conventional, VA, FHA, or another type of loan. They all require different down payments.

Your Realtor will help you with this process. It is your agent’s job to

- help you find homes for sale

- contact the seller’s agent and make an appointment to show you the home

- make a timely offer

- negotiate directly with the seller’s agent

- oversee the due diligence process while making sure all deadlines are met

- work with title companies, inspectors, and other support professionals

It’s fine to shop for homes on your own. If you are working with an agent (and who wouldn’t, it’s free?) provide him or her with the address of the home, and the Multiple Listing Service (MLS) if you have it.

The seller’s agent and the buyer’s agent will divide the commission for the home

In most cases, the seller pays a percentage of the gross sale to the seller’s agent. From there, it is divided according to the agents’ agreement. In other words, the seller has professional representation. You should too. The seller pays the commission, but the buyer does not.

If you are represented by a professional Realtor, don’t contact the seller’s agent directly. That’s the buyer’s agent’s job.

Make an offer

When you find the home you want, your agent will help you make an offer on the home. He can help you settle on a competitive offer price. An expert negotiator will give it to you straight. He or she will lay out and evaluate your options. Often a seller will counter-offer. Your agent will present counter offers to you, and counter the counter if appropriate. Normally this process takes 1-3 days.

Apply for a mortgage

Because you secured a mortgage prequalification before you started shopping, you are already knee-deep in the process. You will be asked for more verification and documentation. This is when you will find out exactly how much the loan will cost you and how much cash you need to close.

The Truth in Lending Act (TILA) requires that all costs associated with the loan be spelled out to you. If you are counting on only bringing the amount of your down payment to closing, I have some bad news. There are many document fees, filing fees, pre-tax payments, mortgage insurance payments if you are using a Federal Home Administration (FHA) loan and more. Your agent can ask the seller to pay part of the closing costs during Step 4. Some sellers will pay upfront for a home warranty policy.

This process can be a little nerve-wracking. But if you have your ducks lined up, it will be much easier. The lender will disclose and itemize every expense. Review that disclosure carefully.

Loan processing usually takes three to four weeks. During that time your Realtor will be busy lining up inspections, requesting repairs, and completing a due diligence process that guarantees you know exactly what you’re getting.

The lender will also order a formal appraisal to make sure the bank knows exactly what it is getting. A title search will be completed and title insurance will be purchased.

Don’t worry, it is good to know all of these steps but you won’t have to do the leg work. That’s what your professional Realtor does.

Close and par-tay!

With four hours before closing, you and your Realtor will do a final walk-through. If there are any unresolved issues, new damage, or items removed from the home that are supposed to be included in the sale, this is the time to speak up.

On closing day, you will meet with representatives of the title company you choose and your lender. You will pay the amount required (check with the title company to clarify acceptable methods of payment before you go). You will also sign many documents. Make sure you understand their contents.

After signing, the lender will transfer the funds to the home seller and initiate your loan. This can take a couple of hours. In some states, it can happen the day after signing.

You will get the keys and enter your new home as arranged in the final documents.